Fine Beautiful Info About Prior Period Errors Disclosure Note Example

Priorperioderrors Accounting Prior Priod Errors Republic Of The

Nice Prior Year Adjustment Disclosure Accounting For Convertible Loan

Prior Period Errors Disclosure Note Example Financial Statement

Ppt Correction Of Errors That Occurred In Previous Periods Powerpoint

Ppt Prior Period Adjustments Due To Corrections Of Errors Years

Ppt International Accounting Standard (ias8) Powerpoint Presentation

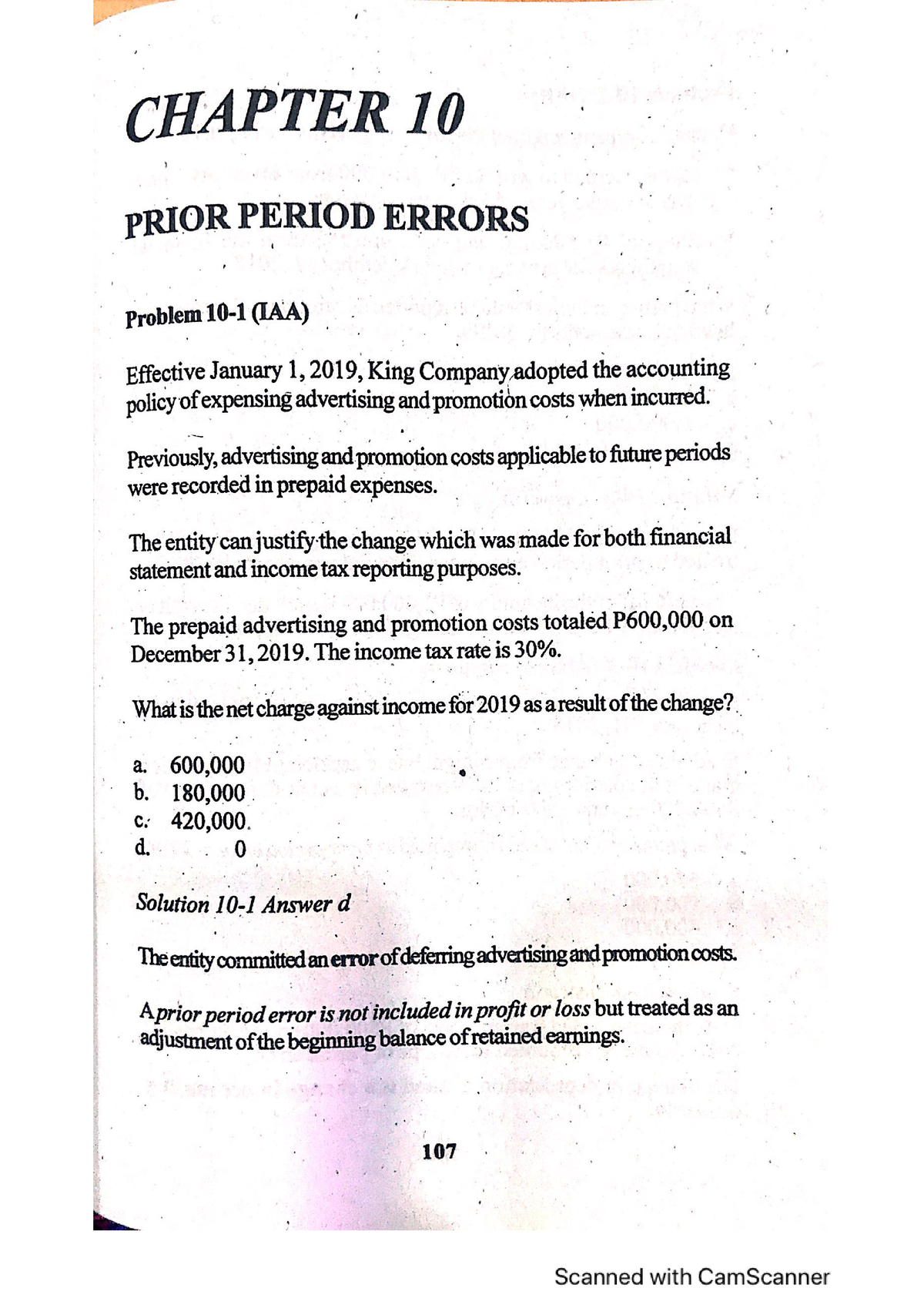

(b) for each prior period presented, to.

Prior period errors disclosure note example. But when should such a correction be made? The prior year comparative figures are presented under the original accounting policies as were applicable at the time of disclosure. The nature of the prior period error;

Account for and disclose the correction of a prior period error in financial statements; Disclosures relating to prior period errors. And are there situations where.

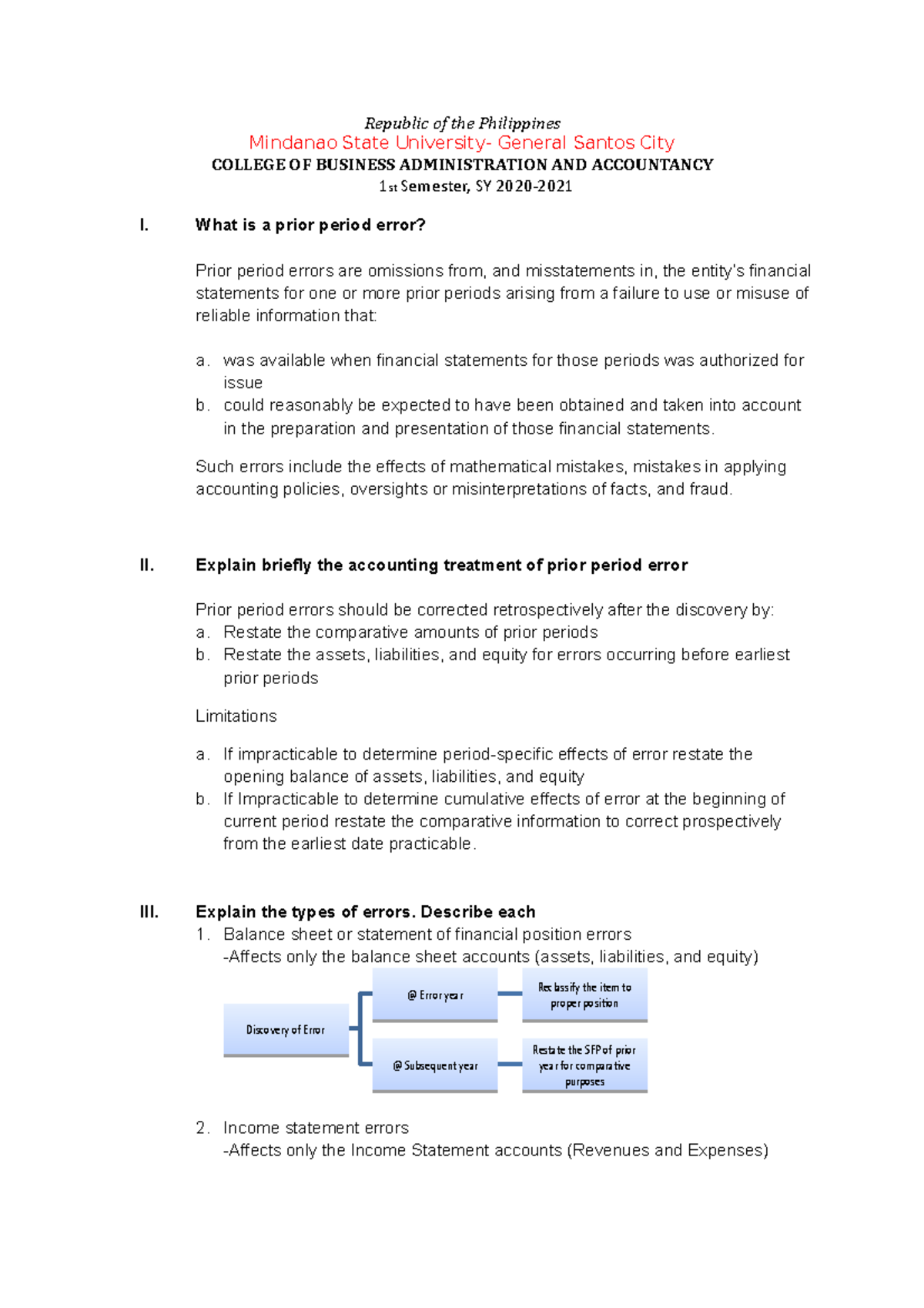

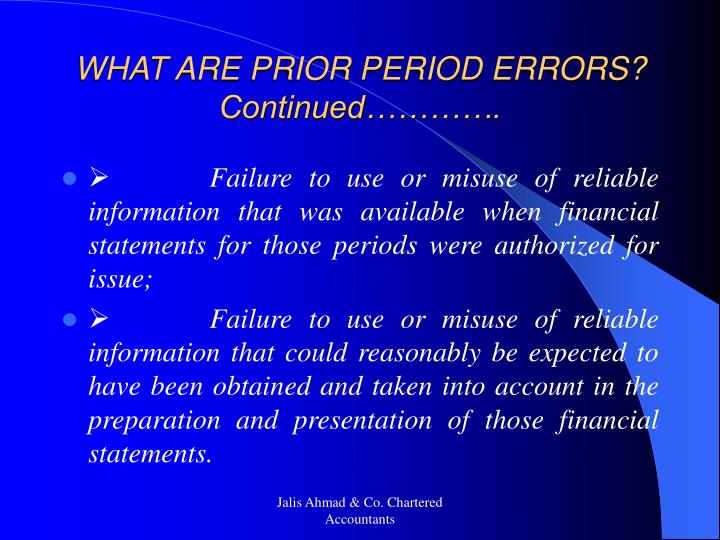

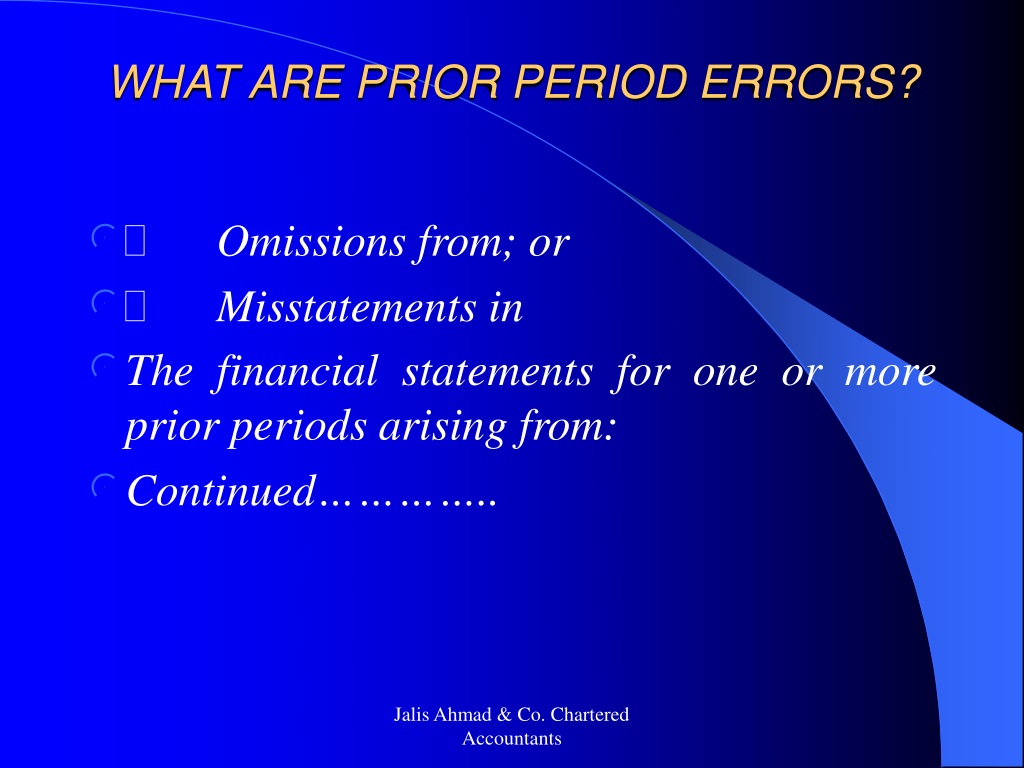

Prior period errors are omissions from, and misstatements in, the agency’s financial statements for one or more prior periods arising from a failure to use, or misuse of,. (a) the nature of the prior period error; Paragraph 10.23 of frs 102 requires the following to be disclosed about material prior period errors:

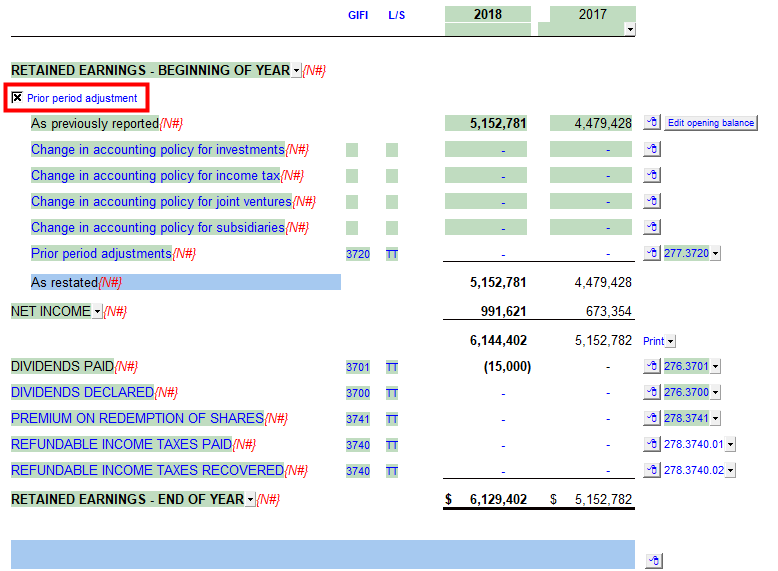

Disclosures relating to prior period errors include: Current year’s profit is therefore. The relevant notes below were included in the.

Prior period errors and adjustments the purpose of this factsheet is to provide guidance on the accounting and disclosure of prior year. Correction of prior period acccounting errors must be performed retrospectively in the financial statements. The nature of the prior period error;

Other material errors 11 2.6 correction of material prior period errors 12 2.7 “impracticable” 12 2.8 more detailed disclosures are required 13 2.9. 2.5 fundamental errors vs. Pensions and other employee benefits.

Demonstrate an understanding of the significant judgements that are required in. Disclosures an entity is required to disclose the nature of and reason for the change in accounting principle, including a discussion of why the new principle is. Correction of errors in the notes to the financial statement:

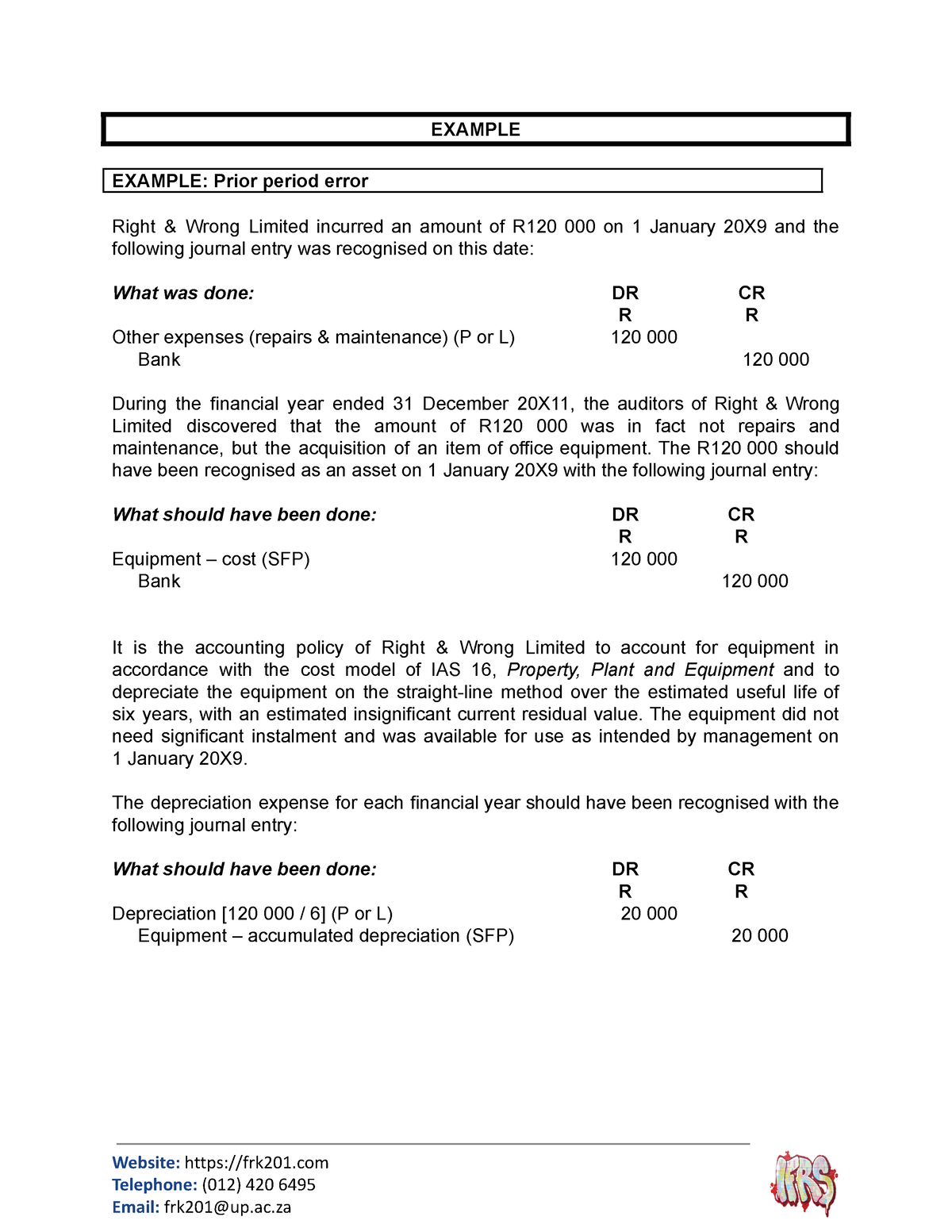

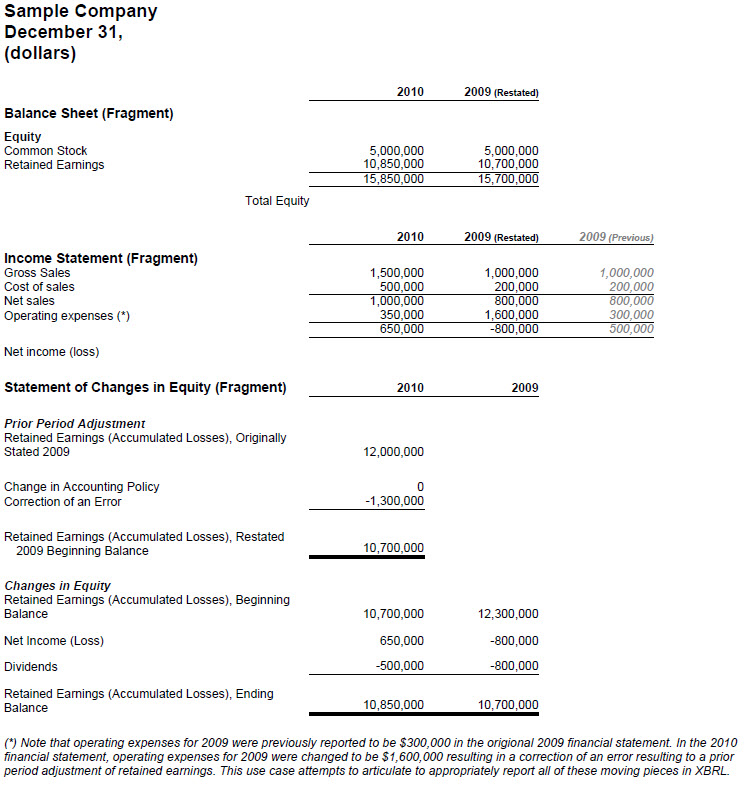

Disclosure of prior period errors. Note that the correction of the error is applied to all prior period comparative amounts affected by the omission (i.e. Example of correction of prior period errors.

For each financial statement line item; An appendix illustrating example disclosures for the early adoption of ifrs 9 financial instruments, taking into account the amendments arising from ifrs 9 financial. For each prior presented, to the extent practicable, the amount of correction:

Disclosing prior period errors. (a) the nature of the prior period error; Overview the purpose of this illustrative guide is to assist departments with the completion of the disclosures required on prior period errors in order to comply with the modified.

Prior Period Adjustment Question. Why Wouldn’t The 2400 Be Subtracted

Ias 8 Handout Examples And Questions Of Example

Prior Period Adjustments

Ppt International Accounting Standard (ias8) Powerpoint Presentation

Prior Period Errors Disclosure Note Example Financial Statement

Prior Period Errors Intermediate Accounting 1 Studocu

Business Use Cases (20170507)

Required Disclosure For Error Restatements Annual Reporting

Roadrunner Transportation Systems (rrts) Investor Presentation

Prior Period Errors Disclosure Note Example Financial Statement

Restatement Of Financial Statements Examples

Acctg Policies And Prior Period Errors Bs Accountancy Studocu

Ppt Accounting Changes And Error Analysis Powerpoint Presentation