Lessons I Learned From Tips About Summary Of Audit Differences

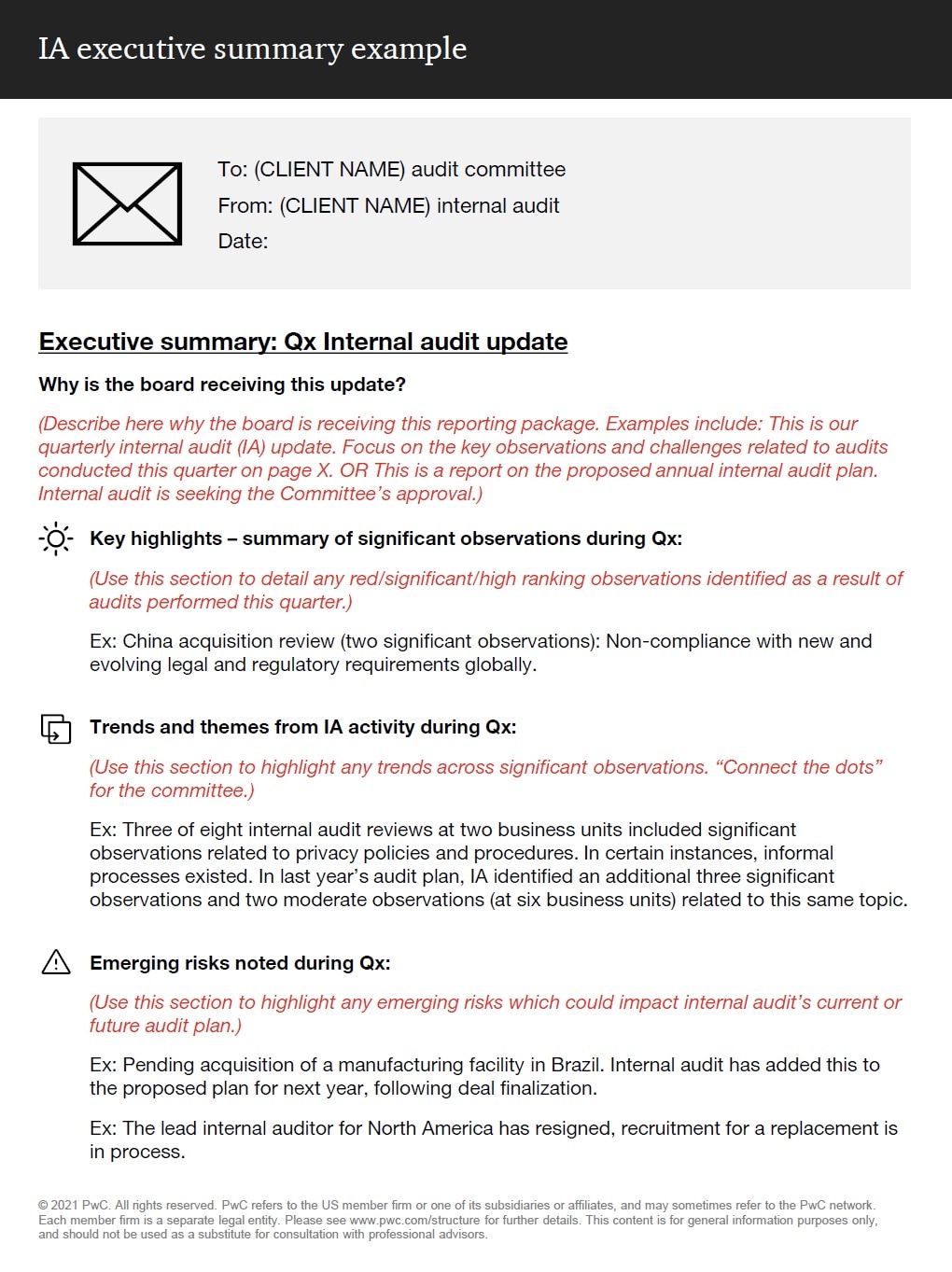

Sample Internal Audit Report Executive Summary Regarding Ssae 16

Auditing I Ch 5 Summary Audit For Chapter

Audit Lean Six Sigma Training Guide Copy

Sample Audit Report Malaysia Sean Howard

Awesome Types Of Audit Letters Hess Law Statement

Favorite Balance Sheet Of Llp Ifrs Latest Standards Accounting For

This article reports the results of an experiment where auditors assess the materiality of audit differences in the same magnitude for both a financial audit and a sustainability (water) assurance engagement.

Summary of audit differences. Introduction at the completion of the audit, the findings need to be reviewed, organized, and presented in a coherent format that can be circulated and reviewed by management as well as other individuals within the organization. Below is an illustration of the summary of adjusted misstatements and the salient features and functions of the workpaper. Confirm with the audit engagement partner that no unresolved matters are likely to have a material effect on the financial statements or auditors' report.

This summary parallels the workpaper documentation currently used in practice and referred to in a variety of different ways, such as a summary of audit differences, a summary of unadjusted differences, or an audit difference evaluation form. An audit refers to an examination of the financial statements of a company. Although the nature of the documentation is somewhat different, both the iaasb and pcaob require auditors to document important judgments in determining the :

Masyarakat untuk kemajuan yudaisme ›. 2 isa 701, communicating key audit matters in the independent auditor’s report An auditor opinion report is a letter that auditors attach to the statutory audit report that reflects their opinion of the audit.

This summary includes all misstated items found throughout the audit that are more significant than de minimis but not considered material. List of dissertations / theses on the topic 'summary of audit differences'. The 4 types of audit opinions.

Journal articles on the topic summary of audit differences: A journal of practice &. A journal of practice & theory 37, no.

Bik, olof, and reggy hooghiemstra. An audit is the review or inspection of a company or individual's accounts by an independent body. In this lesson, learn about how to use internal audit results to improve the risk position of the department, including identification of trends, summarizing results, and providing an adequate.

A brief description every time an audit concludes, an auditor is required to present a summary of misstatements, sometimes referred to as a summary of past adjustments. To make it easy we can make a summary which follows the audit process flowchart above as in the table below: Review a summary of unadjusted audit differences.

Auditors can choose among four different types of auditor opinion reports. Read the financial statements and auditors' report. The output of this process is the audit summary report (asr).

The audit committee is a standing committee of the board of directors, charged with overseeing the company’s financial reporting processes and internal control over financial reporting (icfr) and the audits of the company’s financial statements. Definisi dari sad, apa sad berarti, yang berarti sad, ringkasan audit perbedaan, singkatan sad dari ringkasan audit perbedaan. Written by cfi team what is an audit?

Essentially, a compilation requires the auditor to simply present financial statements based on the representations made by management, with no. This article describes and discusses the requirements of isa 450, evaluation of misstatements identified during the audit and provides some examples of the application of the isa in the context of the advanced audit and assurance exam. For each matter arising from the audit of the financial statements that:

E&c Module 8

How To Write An Audit Report Summary

Iso/iec 170252017 Required Documentation In 2020 Laboratory

What Did We Find? Office Of The Auditor General

Concept Of Flexible Internal Audit Differences From Traditional

Prepare For Your Audit! Steps 5 & 6 Review And Submit Audit Edtec

Audit Free Of Charge Creative Commons Handwriting Image

Audit Summary Template Beautiful 7 Sample External Reports Docs

Sample Of Auditing Report Capriartfilmfestival Internal Audit

Audit Report Template Report, Audit,

Ppt Audit Sampling For Tests Of Controls And Substantive

Internal Summary Audit Report In Word And Pdf Formats Page 2 Of

How To Write An Audit