Exemplary Info About Difference Between General Purpose And Special Financial Statements

Accounting 101 Objectives And Users Of The General Purpose Financial

Ace Difference Between General Purpose And Special Financial Statements

Special Purpose Financial Statements New Reporting Regime

Purpose Of Financial Statements Objectives

Difference Between General Purpose Computer And Special

Accounting 101 Components Of The General Purpose Financial Statements

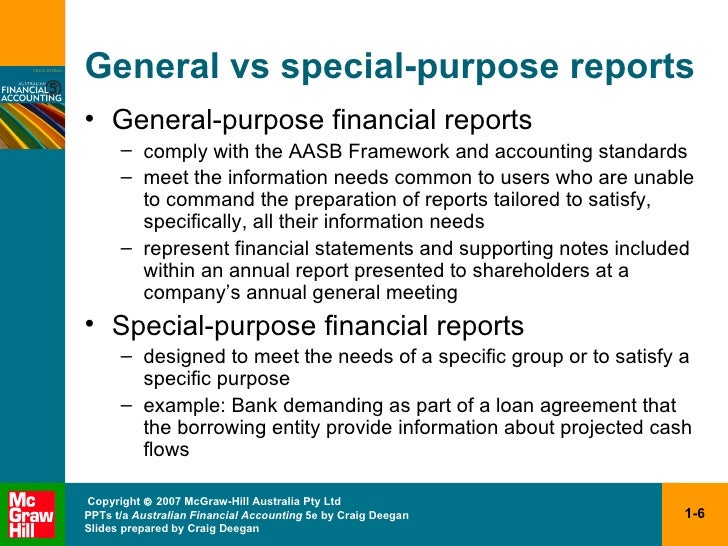

General purpose financial statements versus special purpose financial statements the reporting entity concept and the concept of general purpose financial statements.

Difference between general purpose and special purpose financial statements. These statements are tailored to meet the unique needs of particular stakeholders, such as. 2022 will be the year that marks the death of special. Can you explain the difference between general purpose financial reports (gpfr) and special purpose financial reports (spfr)?

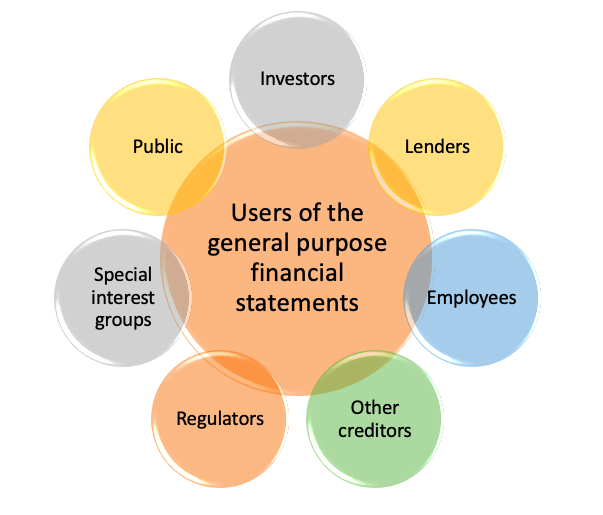

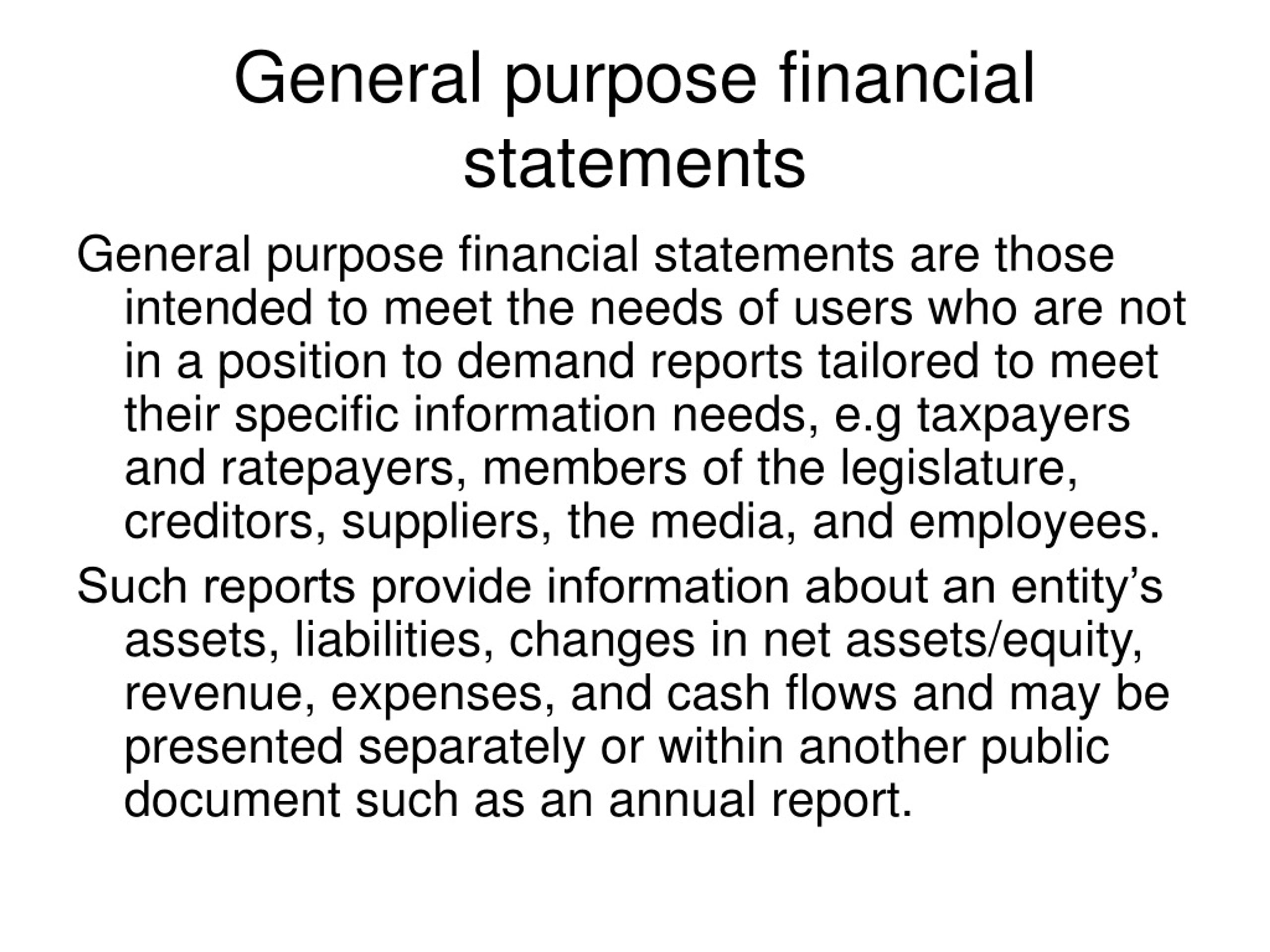

Consolidated reports for service providers. This technical q&a answers: General purpose financial statements are defined in “aasb 101 presentation of financial statements” as “those intended to meet the needs of users.

The 'two out of three' rule. General purpose financial reports. What is the authoritative guidance for financial statements prepared under a special purpose framework?

Gaap includes volumes of authoritative. When preparing tax basis financial statements, how are differences between u.s. Type of service that must provide this.

The general rule is that if the financial statements are. Financial reports created to present financial information to a select audience are known as special purpose financial statements. The table below highlights the significant disclosure differences between general purpose financial statements (gpfs) prepared under the new aasb 1060, gpfs prepared.

Published jun 4, 2023. General purpose financial statements (gpfs) are prepared for a wide range of users, including investors, creditors, and other. Gpfs are designed for a wide audience and provide a comprehensive view of a company’s financial condition, while spfs are designed for a specific purpose or.

Financial statements considered to be special purpose financial are still statements for purposes of the isas. Gaap and irs rules handled? In contrast, special purpose financial statements are prepared for specific users or purposes beyond the scope of general reporting requirements.

Difference Between General Purpose Computer And Special

Changes To Special Purpose Financial Statements Reporting Wlf

Ppt Ipsas 24 Powerpoint Presentation, Free Download Id9086008

Ace Difference Between General Purpose And Special Financial Statements

Difference Between General Purpose Financial Statement And Special

Special Purpose Vs General Financial Statements Vincents

What Are General Purpose Financial Statements? Superfastcpa Cpa Review

Ace Difference Between General Purpose And Special Financial Statements

General Purpose And Special Financial Statements

Removal Of Special Purpose Financial Statements Dfk Benjamin King Money

Accounting 101 Objectives And Users Of The General Purpose Financial

Deegan5e Ch01