Fun Info About Modified Audit Opinion

Modified Audit Opinions And Financial Constraints. Download Table

Modified Opinion Audit Report Example Financial Statement Alayneabrahams

(pdf) Do Modified Audit Opinions Have Economic Consequences? Empirical

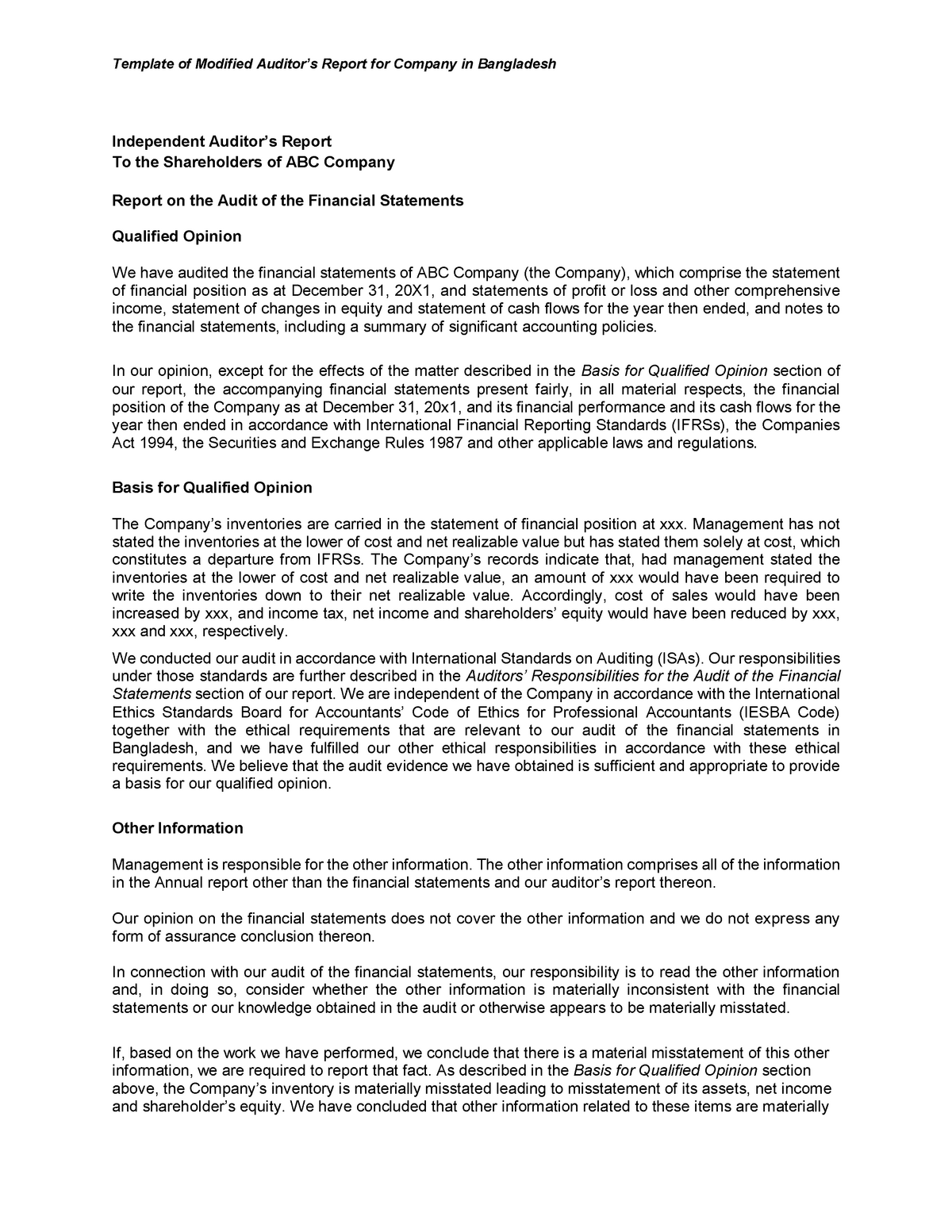

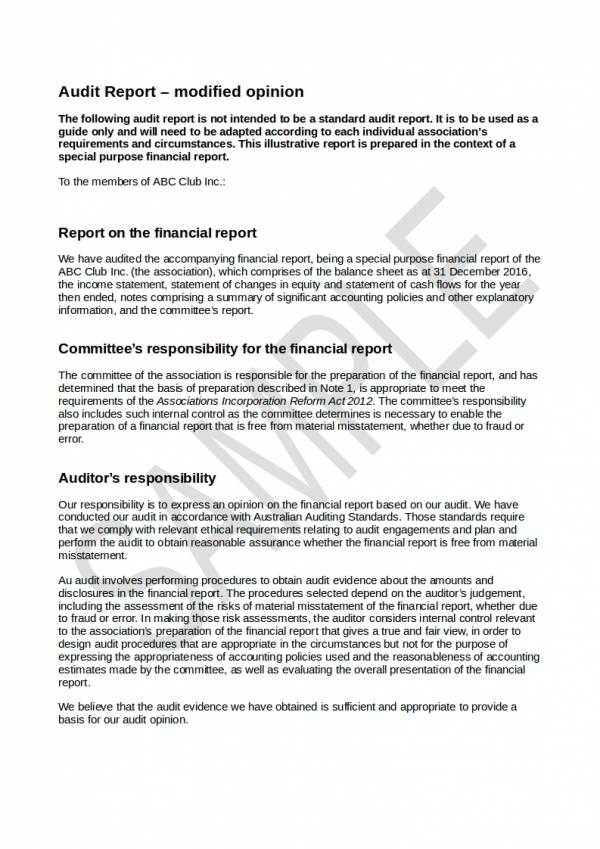

Tamplate Of Modified Auditor's Report For Company In Bangladesh

3.2 Audit Report Notes In Accordance With Acca 3

Modified Audit Reports Past Questions Youtube

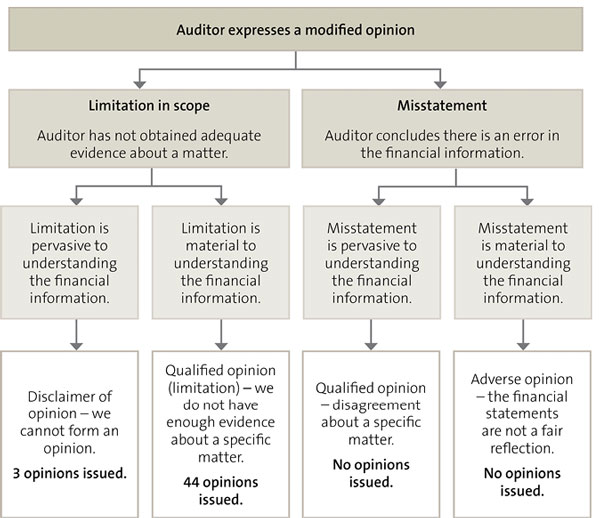

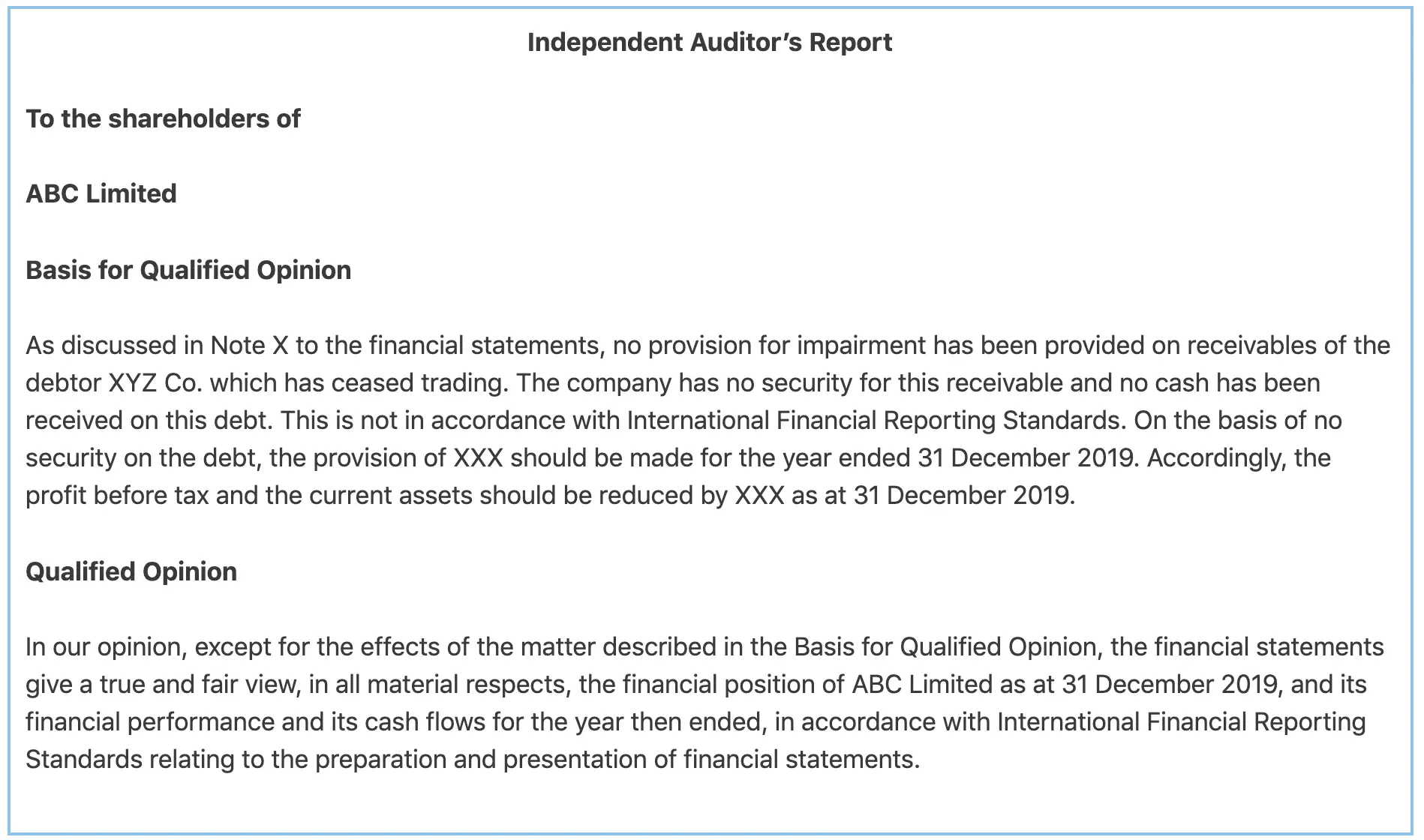

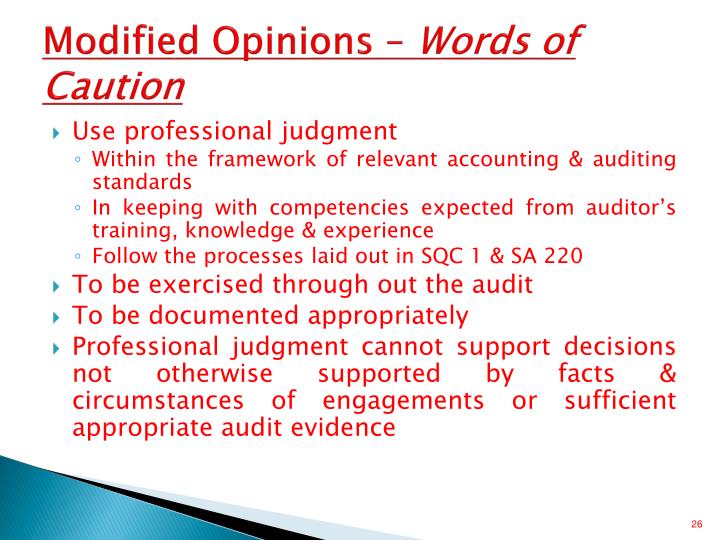

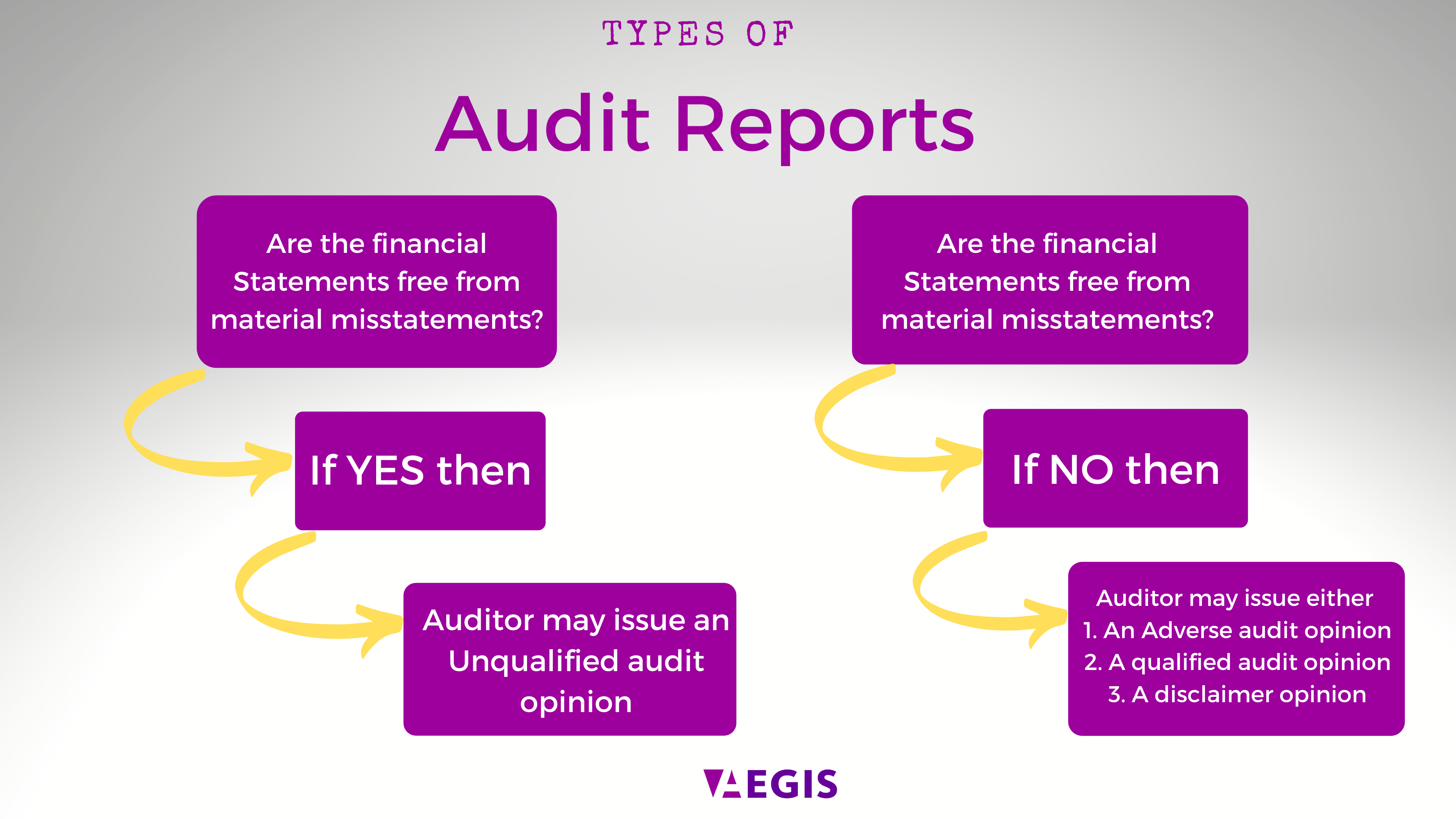

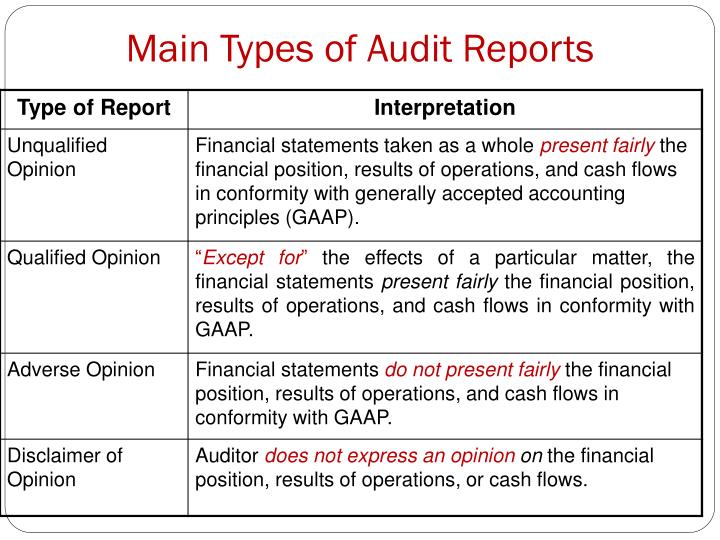

Based on isa 705, modification to the opinion in the independent auditors’ report, there are three modified audit opinions:

Modified audit opinion. There are three types of modification. 1 singapore standard on auditing ssa 705 (revised) modifications to the opinion in the independent auditor’s report ssa 705 was issued in january 2010. Find out the reasons, materiality,.

In addition, out of the fear of losing. This international standard on auditing (isa) deals with the auditor’s responsibility to issue an appropriate report in circumstances when, in forming an opinion in accordance with. As a direct consequence, audit opinions may be modified in the following ways and provides a brief explanation of each:

Modified audit opinion has been largely based on opinion shopping, that is, the likelihood of auditor turnover following maos (lu & tong ,2003;li &wu,2002;huang,2010) [1,2,3]. Their use depends upon the nature and severity of the matter under consideration. (i) qualified (ii) adverse (iii) disclaimer.

Usually, a modified opinion will be described as qualified, adverse, or given as a disclaimer of opinion. Types of modified opinions.02 this section establishes three types of modified opinions, namely, a qualified opinion,an adverse opinion,and a disclaimer of. International standard on auditing 705 modifications to the opinion in the independent auditor’s report (effective for audits of financial statements.

When the auditor modifies the audit opinion, the auditor shall use the heading “qualified opinion,” “adverse opinion,” or “disclaimer of opinion,” as appropriate, for the. Technical helpsheet issued to help icaew members to identify the various changes that may need to be made to audit reports under international standards of. If modified audit opinions have an adverse impact on credit availability, one would expect that a change from having institutional debt to not having institutional.

Types of modified opinions 2. This sa establishes three types of modified opinions, namely, a qualified opinion, an adverse opinion, and a disclaimer of opinion. Usually, a modified opinion will be described as qualified, adverse, or given as a disclaimer of opinion.

Learn how to modify an audit opinion when the auditor concludes that the financial statements are materially or pervasively misstated. When the auditor modifies the audit opinion, the auditor shall use the heading qualified opinion, adverse opinion, or disclaimer of opinion, as appropriate, for the. The purpose of this paper is to review the empirical literature on value relevance of audit reports by providing current evidence on the market reaction to.

The qualified opinion the adverse opinion the.

Ppt New Audit Reporting Standards Powerpoint Presentation Id1555836

Audit Report Qualified Opinion Impact Of

Modified Audit Opinion

Free 17+ Financial Audit Report Samples Templates In Pdf Ms Word Pages

Audit Opinion Types Available In Our Europe Database Arc

(pdf) Analysis Of Going Concern Modified Audit Report In Indonesia And

Ppt Advanced Auditing Powerpoint Presentation Id2611463

Modified Audit Opinions Determining Which Is Appropriate Cpa Hall Talk

Modified Audit Report Vs Opinion Youtube

The Difference Between Modified Audit Opinion And Report

(pdf) Board Structure And Modified Audit Opinions The Case Of